Let’s be honest, buying a home is rarely just about square footage or location. It’s emotional. You walk into a flat, picture your furniture, imagine weekend mornings with tea on the balcony… and suddenly, it feels like this is it. But right after that excitement comes a very practical question: “Can I really afford this?”

That’s where the HDFC Home Loan EMI Calculator quietly becomes one of the most useful tools you’ll ever use during your home-buying journey. Before you commit to anything, it helps you understand what your monthly payments might look like, no guesswork, no assumptions.

In India, a home loan often runs for 15–25 years. That’s a long relationship with your bank. So, knowing your EMI in advance isn’t just helpful, it’s necessary. It allows you to plan your finances without stretching yourself too thin or compromising your lifestyle later on.

What is the HDFC Home Loan EMI Calculator?

Think of it like a quick reality check, but a helpful one.

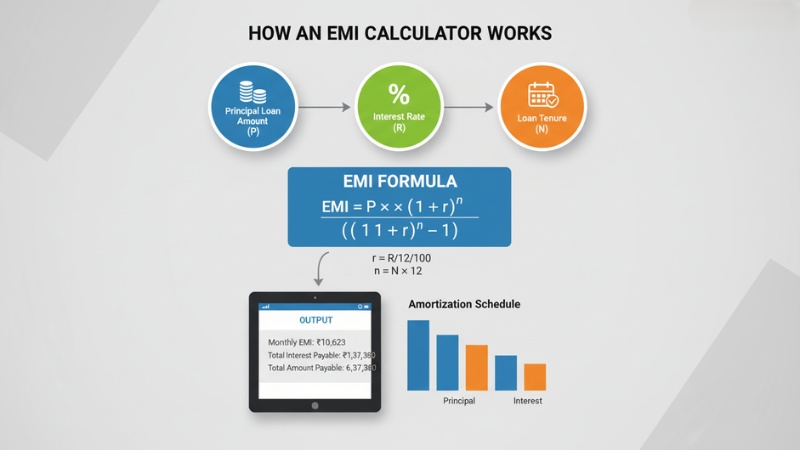

The calculator is an online tool that tells you how much EMI (Equated Monthly Installment) you’ll be paying every month based on a few basic inputs. Instead of manually calculating or depending on rough estimates from agents, you get a number that’s much closer to reality.

You simply enter your loan amount, interest rate, and repayment period. Within seconds, the tool gives you a monthly figure.

What makes the home loan calculator HDFC especially useful is that it allows you to play around with numbers. Not happy with the EMI? Adjust the tenure. Want to see how a bigger down payment helps? Try it instantly. It gives you flexibility, and more importantly, clarity.

How Does an EMI Calculator Work?

At first glance, EMI calculations might sound technical, but they’re actually based on three simple things:

Loan Amount

This is the amount you borrow from the bank. If you’re buying a ₹1 crore property and paying ₹20 lakh upfront, your loan amount will be ₹80 lakh. Naturally, the bigger the loan, the higher your EMI.

Interest Rate

This is what the bank charges you for lending money. Even a difference of 0.5% can change your EMI noticeably over time.

Tenure

This is how long it takes you to repay the loan. A longer tenure means smaller EMIs, but you’ll end up paying more interest overall. A shorter tenure increases your EMI but reduces total interest.

The calculator combines these three and shows you your monthly obligation. No complicated formulas, no confusion, just a clear number you can work with.

Step-by-Step Guide to Use the Calculator

If you’ve never used an EMI calculator before, don’t worry, it’s very straightforward.

-

Start by entering the loan amount you’re considering

-

Add the interest rate (you can check current rates online)

-

Choose the number of years you want to repay the loan

-

Hit calculate

That’s it. The real advantage is that you can experiment. Increase your down payment slightly and see what happens. Reduce tenure and check the difference. Within a few minutes, you’ll have a much better understanding of what works for you.

Benefits of Using HDFC EMI Calculator

You might wonder, why not just ask a bank or agent? Well, you can. But having your own estimate gives you control.

It Saves Time

You don’t need multiple meetings or follow-ups. Just enter your details, and you’re done in seconds.

It Helps You Stay Realistic

Sometimes we overestimate what we can afford. Seeing an actual EMI number brings you back to reality in a good way.

It Makes Budgeting Easier

When you know your EMI, you can plan everything else, expenses, savings, and even vacations.

It Lets You Compare Options

Thinking of choosing between two properties? Just change the loan amount and see how your EMI changes. Simple.

Why EMI Planning is Crucial Before Buying Property

Many people make the mistake of choosing a home first and figuring out their finances later. It feels exciting in the moment, but it can lead to stress later.

Let’s say you’re exploring luxury flats in Chandigarh. The lifestyle is appealing, with modern amenities, a better location, and a sense of upgrade. But these homes also come with higher EMIs.

Now consider the difference between 3 BHK Luxury flats in Mohali and 4 BHK Luxury flats in Mohali. On paper, the jump may seem manageable. But when you calculate EMI, that extra room might increase your monthly burden more than expected.

This is why EMI planning matters. It helps you decide not just what you want, but what you can comfortably manage over the long term. Because at the end of the day, your home should bring peace, not financial pressure.

A Real Example of Smart Home Buying in Mohali

If you’re exploring premium living options in the Tricity, Beverly Golf Avenue is a great example of how modern homebuyers are making informed decisions. Located in Sector 65, Mohali, this residential project offers thoughtfully designed 3 and 4 BHK luxury apartments with spacious layouts, high-end amenities, and a peaceful environment close to Chandigarh.

What makes it even more relevant for buyers today is the combination of lifestyle and practicality. With features like a clubhouse, swimming pool, landscaped greens, and even access to a golf range, it reflects the growing demand for comfort-driven living.

But more importantly, properties like these highlight why EMI planning matters. When you’re considering premium homes, understanding your monthly financial commitment beforehand ensures that you enjoy the lifestyle without unnecessary financial pressure. It’s not just about choosing a luxury home—it’s about choosing one that fits your budget comfortably.

Fixed vs Floating Interest Rates: What Should You Choose?

When you take a home loan, one of the first decisions you’ll face is choosing between a fixed and a floating interest rate. At first, it might seem like a technical choice, but it actually has a direct impact on your monthly EMI and long-term financial comfort.

A fixed interest rate means your EMI stays the same throughout the loan tenure. This can be reassuring, especially if you prefer stability and want to plan your finances without worrying about market changes. It’s a good option if you like predictability and don’t want surprises.

On the other hand, a floating interest rate changes based on market conditions. If interest rates go down, your EMI may reduce, which can save you money over time. But if rates increase, your EMI could go up as well.

There’s no one-size-fits-all answer here. If you value stability, fixed might work better. If you’re comfortable with some fluctuation and want to benefit from potential rate cuts, floating could be the smarter choice. Many buyers today lean towards floating rates, but the right decision depends on your financial situation and risk comfort.

How Your Credit Score Affects Home Loan EMI

Your credit score might seem like just a number, but when it comes to home loans, it plays a bigger role than most people expect.

Banks use your credit score to assess how reliable you are as a borrower. A higher score usually means lower risk for the lender, which often translates into better interest rates for you. And even a slightly lower interest rate can make a noticeable difference in your EMI.

For example, if two people apply for the same loan amount but have different credit scores, the one with the higher score is more likely to get a lower interest rate, and therefore a lower EMI.

If your score is on the lower side, it doesn’t mean you won’t get a loan. But you might end up paying more over time. That’s why it’s a good idea to check your credit score before applying and, if needed, take a little time to improve it.

Simple steps like paying your bills on time, reducing outstanding debt, and avoiding multiple loan applications can help boost your score and put you in a better position when applying for a home loan.

Hidden Costs in Home Loans You Should Not Ignore

When planning for a home loan, most people focus only on the EMI. But in reality, there are several additional costs that can catch you off guard if you’re not prepared.

For starters, there’s the processing fee charged by the bank. Then you have legal and technical verification charges, which are part of the loan approval process. These may seem small individually, but together they can add up.

You’ll also need to consider property-related expenses like registration charges, stamp duty, and maintenance deposits. And if you’re buying a ready-to-move-in property, there could be society charges or advance maintenance costs as well.

Another aspect many people overlook is home loan insurance. While it’s optional, some lenders recommend or bundle it with the loan, adding to your overall cost.

The key here is simple: don’t just calculate your EMI. Look at the bigger picture. Understanding these hidden costs in advance ensures that you’re financially prepared and won’t face any unexpected pressure later on.

Smart Tips to Reduce Your Home Loan EMI

If your EMI feels higher than expected, don’t panic. There are practical ways to bring it down.

First, try increasing your down payment. Even a small increase can reduce your loan amount significantly.

Second, choose your tenure wisely. Many people go for the longest tenure just to reduce EMI, but that increases total interest. Find a middle ground.

Third, compare interest rates before finalizing your loan. Don’t just settle for the first offer.

And lastly, consider making occasional prepayments. Even one extra payment a year can reduce your overall burden.

Common Mistakes to Avoid

Even smart buyers sometimes slip up. Here are a few things to watch out for:

Ignoring extra costs like maintenance, registration, and interiors. These add up quickly.

Taking the maximum loan offered by the bank. Just because you’re eligible doesn’t mean it’s comfortable.

Skipping EMI calculation entirely. This is more common than you think, and it often leads to regret later.

A little caution here can save you years of financial stress.

Real-Life Example

Let me put this into perspective with a simple example.

A friend of mine was planning to buy a flat worth ₹75 lakh. He was comfortable with the idea until he actually calculated the EMI.

With a loan of around ₹55 lakh at 8.5% for 20 years, his EMI came close to ₹48,000 per month.

At first, he thought it was manageable. But when he looked at his monthly expenses, rent, groceries, and family needs, it felt tight.

So, he adjusted his plan. He increased his down payment slightly and extended the tenure by a few years. The EMI dropped to a more comfortable level, and he could move forward without stress.

That’s the difference planning makes.

Frequently Asked Questions

1. What exactly is an EMI?

It’s the fixed monthly amount you pay towards your home loan, including both principal and interest.

2. Is the calculator reliable?

Yes, it gives a close estimate. Final EMI may vary slightly depending on lender terms.

3. Can my EMI change later?

If you choose a floating interest rate, your EMI can increase or decrease.

4. How much EMI is safe?

Ideally, keep it within 30–40% of your monthly income.

5. Should I prepay my loan?

If you have extra funds, prepayment can reduce your loan burden.

6. Does tenure really matter?

Yes, it directly affects both your EMI and total interest paid.

7. Can I use the calculator multiple times?

You should. Trying different scenarios helps you make better decisions.

8. Is EMI planning really that important?

Absolutely. It’s the foundation of a stress-free home-buying experience.

Conclusion

At the end of the day, buying a home is one of the biggest financial decisions you’ll make. It’s not just about choosing the right location or layout; it’s about making sure your finances can support that decision comfortably over time, especially when you’re considering options like luxury flats Chandigarh.

That’s why tools like the HDFC Home Loan EMI Calculator are so valuable. They give you clarity before commitment. They help you understand your limits, explore your options, and move forward with confidence.

So before you finalize that dream property, whether it’s a modern apartment or a spacious upgrade, take a few minutes to calculate your EMI. It might seem like a small step, but it can make a huge difference in how stress-free your homeownership journey turns out to be.